Presented to Parliament by the Secretary of State for Business, Energy and Industrial Strategy by Command of Her Majesty.

February 2022

Command paper CP 638

Ministerial foreword

It is right the experiment should be tried; and, in my judgment, the principle we should adopt is this – not to throw the slightest obstacle in the way of limited companies being formed – because the effect of that would be to arrest niney-nine good schemes in order that the bad hundredth might be prevented; but to allow them all to come into existence, and when difficulties arise, to arm the courts of justice with sufficient powers to check extravagance or roguery in the management of companies, and to save them from the wreck in which they may be involved.

(Robert Lowe, Vice President of the Board of Trade, introducing the Joint Stock Companies Bill to Parliament, 1 February 1856)

Companies House operates the UK’s open, flexible corporate registration framework. It provides the UK’s business community with a simple system for creating and maintaining companies and other legal entities, and publicising information on those entities for the benefit of investors, lenders, regulators and the public. These roles facilitate economic activity across the UK, and the companies register is accessed over 10 billion times a year, informing many business and lending decisions. It is an important foundation of the UK’s business environment.

However, recent years have seen this framework manipulated, particularly in the use of anonymous or fraudulent ‘shell’ companies and partnerships. These provide criminals with a veneer of legitimacy to help commit a range of crimes, from grand corruption and money laundering to fraud and identity theft. This undermines our standing as a free, open and trustworthy democracy and undermines the UK’s reputation as a great place to do business

The government is determined to stop this abuse. At the same time, we will maintain our user-friendly, low-cost framework. We consulted on a broad range of potential measures in 2019, receiving over 1,300 responses, and announced high-level plans for reform in 2020. Shortly afterwards we published 3 further consultations on important areas of detail, including on areas not covered by the original consultation and where the business community had asked us to consider additional action. These also received a broad and positive response, and I am therefore confident that we have found a sensible and balanced way forward.

Since those consultations, the importance of Companies House reform as a foundation of our open and resilient economy was highlighted in the Integrated Review of Security, Defence, Development and Foreign Policy. Ongoing geopolitical events have reinforced the need to combat dirty money flowing into the Western financial system from former Soviet countries. And I am acutely aware that ordinary people continue to find themselves victims of fraud through no fault of their own due to the limitations of the current legislation.

This paper sets out the government’s final position on the reforms ahead of introducing legislation. It provides considerably more detail on the way the reforms will operate and includes responses to the 3 consultations we ran last winter. I hope it will help the UK’s business community, law enforcement agencies and all stakeholders start to prepare for the changes to come.

In the meantime, investment is already flowing. In the Autumn 2021 Budget, the government committed £63 million to transforming every aspect of Companies House operations to deliver on its new responsibilities. Companies House will transform its digital capabilities and improve user experience to better serve the needs of a thriving 21st century economy.

The combination of legislative and operational reform will make Companies House fit for the future. Alongside other related measures, they will help safeguard our national security, reduce the economic and social costs of fraud, and deliver real benefits to the whole business community. They are a step towards us making the UK’s economy the best regulated in the world.

Lord Callanan

Parliamentary Under-Secretary of State for Business, Energy and Corporate Responsibility

Part 1 – Introduction

1. Companies House performs 2 vital roles which underpin the UK’s strong, transparent and attractive business environment. It facilitates the creation of limited companies and a range of other legal entities, which are vital building blocks of the modern economy. And it provides – free of charge and online – information about those entities, for the benefit of investors, providers of finance and other creditors, government agencies and the general public. Formally, powers are vested in the Registrar of Companies for England and Wales (and equivalent Registrars for Scotland and for Northern Ireland), who is supported in her work by the staff of Companies House, an Executive Agency of the Department for Business, Energy and Industrial Strategy.

2. Companies House incorporates hundreds of thousands of companies each year. Incorporation provides shareholders with limited liability for the debts of the company – shareholders are only liable up to the amount, if any, unpaid on shares they own in the company – and establishes a company as a legal person separate from its owners. The combination of limited liability and legal personality provides those running companies with the freedom to take risks in the knowledge that they will not be personally liable for the company’s debts. This enables entrepreneurs across the economy to establish and grow businesses and has been an essential element of the UK economy since the mid-19th Century.

3. Those wishing to incorporate a company in the UK can do so quickly and very cheaply. In 2020-21 Companies House incorporated 810,316 companies. Companies House incorporation fees are among the lowest in the world and 99% of incorporation applications are processed within 24 hours. The total value of incorporation to owners of limited liability companies with 0 to 9 employees is estimated at £9.6 billion. [footnote 1]

4. Companies House makes company information public on the companies register. [footnote 2] Companies must provide the Registrar of Companies with information on their ownership and financial position. This is a fundamental component of good governance for businesses in the UK. From its origins in the Joint Stock Companies Act 1856 to its modern successor the Companies Act 2006, company law in the UK has always regarded transparency as the price of limited liability.

5. Since 2015, the vast majority of the information on the register has been free to access for everyone. It was accessed more than 10.2 billion times in 2020-2021 (up from 668 million in 2012-13). Research suggests the register is worth £1-3 billion to the UK [footnote 3] economy, informing many business and lending decisions and helping the owners and directors of companies be held to account.

Companies House: Key statistics

There are currently 4.4 million active companies registered with Companies House (with the vast majority small or micro) and ~650,000 incorporations each year

- 2.8 million registered companies in 2012/13

- 4.4 million registered companies in 2020/21

£12 to incorporate:

- 99% within 24 hours

Incorporating a company with Companies House is low cost and quick.

Since the creation of the free, online public companies register in 2015, searches have increased significantly:

- 1.3 billion register searches in 2015/16

- 10.2 billion register searches in 2020/21

£1-3 billion – Value of Company Register data in 2018.

BEIS research valued Companies House data at between £1-3 billion per year in 2018, with financial information the most valuable information to users

£9.6 billion – Value of company incorporation to Limited Liability owners with 0-9 employees.

BEIS research from 2021 finds evidence business owners highly value being able to incorporate, with limited liability the main benefit

The case for change

6. Companies House has a strong track record for customer service and is well regarded worldwide. However, the legal framework that it operates in needs updating to meet the demands of a thriving and increasingly digitally-based 21st century economy. More fundamentally, the government would like to see Companies House play an expanded role so will change its statutory role from being a largely passive recipient of information to a much more active gatekeeper over company creation and custodian of more reliable data.

7. The number of incorporations processed by Companies House each year continues to grow, as does the volume of data it processes – Companies House accepted 12 million transactions last year (a 2.1% increase on last year). Companies House continues to provide outstanding service, last year achieving overall customer satisfaction rate of 86%, but growing demands means Companies House needs investment in its legacy systems to meet the demands of the modern economy.

8. Legislative change will enable Companies House to meet these demands. Companies House will be empowered to require companies to file digitally. This move will digitise Companies House remaining paper-based functions, driving greater efficiency for businesses and Companies House, better value for the money and a more powerful data set for those searching the register.

9. The work of Companies House is well regarded worldwide in international assessments for transparency over corporate entities. In December 2018 the Financial Action Task Force (FATF), in their mutual evaluation report on anti-money laundering and counter-terrorist financing measures, assessed the UK as one of a small minority of countries having a substantially effective framework for transparency over corporate entities in terms of preventing their misuse for money laundering and terrorist finance. [footnote 4]

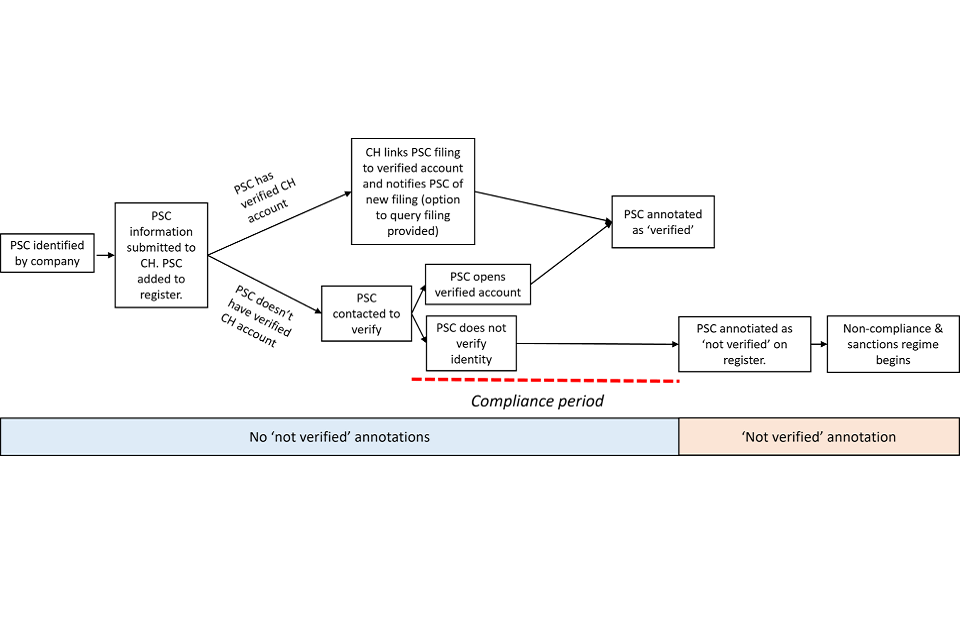

10. Nevertheless, recent years have seen growing instances of misuse of companies, concerns over the accuracy of the companies register and challenges safeguarding personal data on the register. In parallel, a number of stakeholders have drawn attention to the opportunity for Companies House to play a greater role tackling economic crime, working in partnership with other agencies and the private sector.

11. It was for these reasons that the government consulted on potential reform in 2019, receiving over 1,300 responses, the majority of which supported reform. There is a clear consensus across business and professional groups, law enforcement agencies and civil society groups that reform is needed.

12. The government published its response in September 2020, confirming we intend to legislate to significantly strengthen our corporate registration framework, and announcing the biggest changes in the role of the Registrar since it was created in 1844. [footnote 5] Alongside this, Companies House will undergo a full transformation, with the ambition of being the most innovative, open and trusted registry in the world. We plan to improve Companies House’s contribution to the UK economy, and at the same time boost Companies House capacity to combat economic crime.

13. Significant policy development has followed since September 2020, including 3 further consultations examining detailed proposals on the powers of the Registrar [footnote 6], implementation of the ban on corporate directors [footnote 7] and improvements to the financial information on the register. [footnote 8]

What changes are we making?

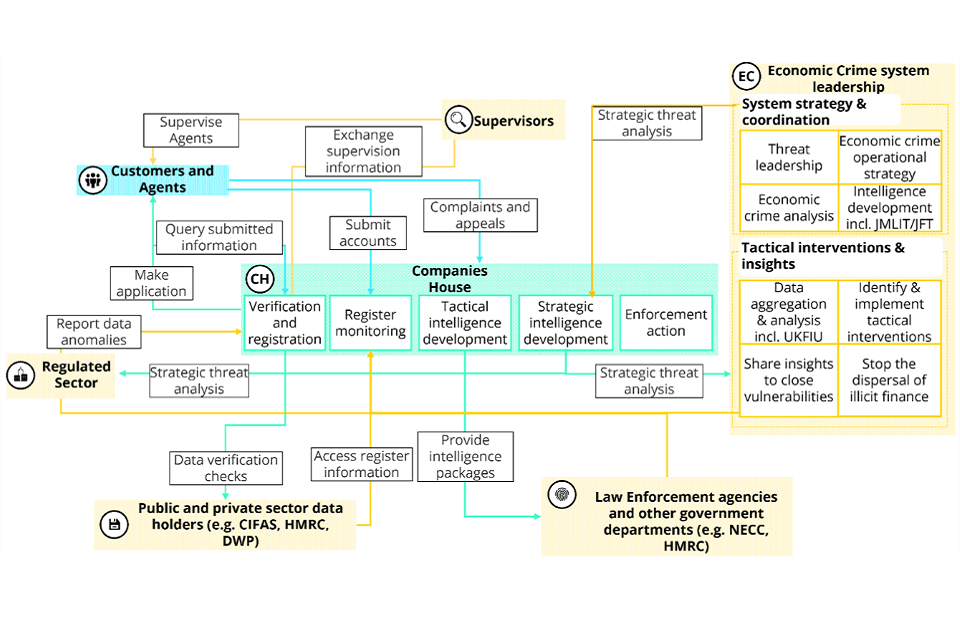

14. The statutory role of the Registrar of Companies (and equivalents in Scotland and Northern Ireland) will expand beyond her current remit of registering company information to include a new function to maintain the integrity of the register of companies and the UK business environment. The Registrar will be equipped with new powers to carry out this function. This will include powers to query suspicious appointments or filings and, in some cases, request further evidence or reject the filing. Companies House will also have more extensive legal gateways for data sharing with law enforcement, other government bodies and the private sector. This will mean more efficient sharing of suspicious activity with law enforcement and establishment of feedback loops with other government bodies and the private sector. This will lead to quicker identification of discrepancies between information on the register and information held by other bodies that can then be questioned by the Registrar’s new powers to query information.

15. Those setting up, managing, and controlling companies and other registrable entities will have a verified identity with Companies House, or have registered and verified their identity via an anti-money laundering supervised third-party agent. This will make anonymous filings harder and discourage those wishing to hide their company ownership through nominees or opaque corporate structures.

16. We will also enhance privacy mechanisms across the register. Anyone whose personal information has been made public on the register in the past will be able to apply to have some of that information suppressed, and we will ensure that individuals who can provide evidence that having their personal information on the public register puts them at risk of harm can apply to have it suppressed.

17. Finally, these reforms are supported by a series of changes to improve the financial information on the register. These are intended to lead to better financial management practices within SMEs, promote the transition to digital reporting, support better business and credit decisions, and help wider efforts to combat economic crime.

18. To deliver the government’s ambition, Companies House will transform every aspect of its skills, culture, operating model, and services. Successful reform will not be possible without this all-encompassing transformation. The government has invested £20 million in the transformation of Companies House in 2021-22 and has committed a further £63 million at the 2021 Spending Review.

19. The combination of legislative and operational reform of Companies House will help ensure the UK is the best place to start and grow a business, and that companies on the UK register are run responsibly, transparently and with accountability. These reforms are a key part of the government’s Economic Crime Plan, and they complement a number of related measures the government has also committed to introducing soon. [footnote 9]

This document

20. This paper sets out the government’s position ahead of introducing legislation into Parliament, bringing to a conclusion the results of further consultation and policy development since September 2020.

21. The first part of this paper sets out the strategic context for this set of reforms. It covers how the reforms to Companies House will contribute to government priorities in national security and anti-corruption, fraud and boosting enterprise.

22. The second part sets out the reforms in greater detail, covering the Companies House transformation, new powers for the Registrar, identity verification, improved privacy protections, greater powers to share data and reforms that will improve the quality of financial information on the register. The annexes contain a full list of the reforms included in this programme and the government responses to the consultations that ran last winter.

Part 2 – Delivering government priorities

Part 2 sets out the outcomes the government intends to deliver through reforms to Companies House and the corporate registration framework:

The reforms to Companies House contribute to 3 key government priorities:

- National security, anti-corruption and organised crime: Recent years have seen reports of thousands of UK companies and partnerships being misused by international money laundering networks. These reforms will help us bear down on the organised criminals, kleptocrats and terrorists that use opaque companies to abuse our financial system and liberal democracy, and to support developing countries to stop the theft of their public assets

- Protecting individuals and businesses from fraud: The social and economic cost of fraud to individuals in England and Wales is £4.7 billion per year [footnote 10] and the cost of organised fraud against businesses and the public sector in the UK is £5.9 billion. [footnote 11] Reform of Companies House will help tackle the use of corporate entities to perpetrate and hide fraud in the UK

- Boosting enterprise: The companies register is a key element of the information architecture of the UK economy and worth £1-3 billion to its users. Reform will make it more reliable and usable helping businesses across the UK economy make better decisions about their suppliers and creditors

Part 2A: National security, anti-corruption and organised crime

23. This part sets how the reforms work in concert to tackle abuse of UK registered companies and partnerships. It sets out examples of how abuse of the UK’s open flexible framework impacts national security, corruption and facilitates organised crime.

How companies and partnerships registered in the UK undermine national security

24. The UK is the fifth largest economy in the world and is currently ranked third in the world for soft power. [footnote 12] Soft power is central to the UK’s international identity as an open, trustworthy, and innovative country. It helps to build positive perceptions of the UK and enhances our ability to attract international business. The UK’s soft power is underpinned by factors including our model of democratic governance, strong legal system, and trustworthy economy.

25. The 2021 Integrated Review highlighted the changing global threat picture, in particular from the shift from a post-Cold War ‘rules-based international system’ to a more fragmented international order, characterised by intensifying competition between states over interests, norms and values. It further emphasised the importance of tackling economic crime and illicit finance, as they fund organised crime groups, terrorists, and other malicious actors.

26. The Integrated Review committed the UK to a range of measures to defend our values at home and abroad. They include a new sanctions regime [footnote 13] specifically targeting corruption, and the National Security and Investment Act 2021 [footnote 14] to maximise the contribution of foreign direct investment to the UK’s economic growth whilst minimising the potential risk to national security.

27. The Integrated Review also recognised that the UK’s openness to the flow of trade, capital, data, ideas, and talent is essential to its long-term prosperity. The speed and low cost associated with incorporating companies in the UK helps maintain our status as a global financial centre and an attractive location for investment. Rapid establishment of legal entities and flexibility over their use is essential not just for entrepreneurs but for the UK’s investment industry and for mergers and acquisitions activity.

28. However, recent evidence shows that our company registration framework has become vulnerable to exploitation by malign actors, corrupt officials and criminals from overseas. In recent years, some thousands of corporate entities registered in the UK have been found to be being used to facilitate major international money laundering schemes (see Case studies 1,2 and 3). There have also been reports of UK companies and partnerships being used to facilitate illegal arms movements, sanctions-busting and financing terrorism.

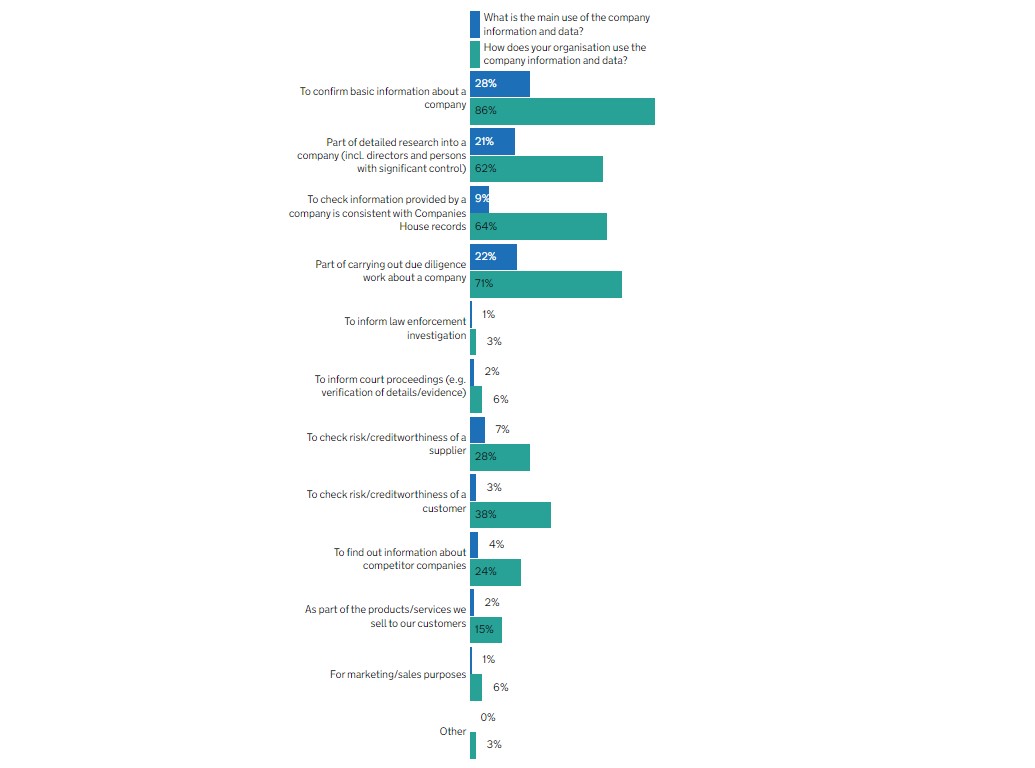

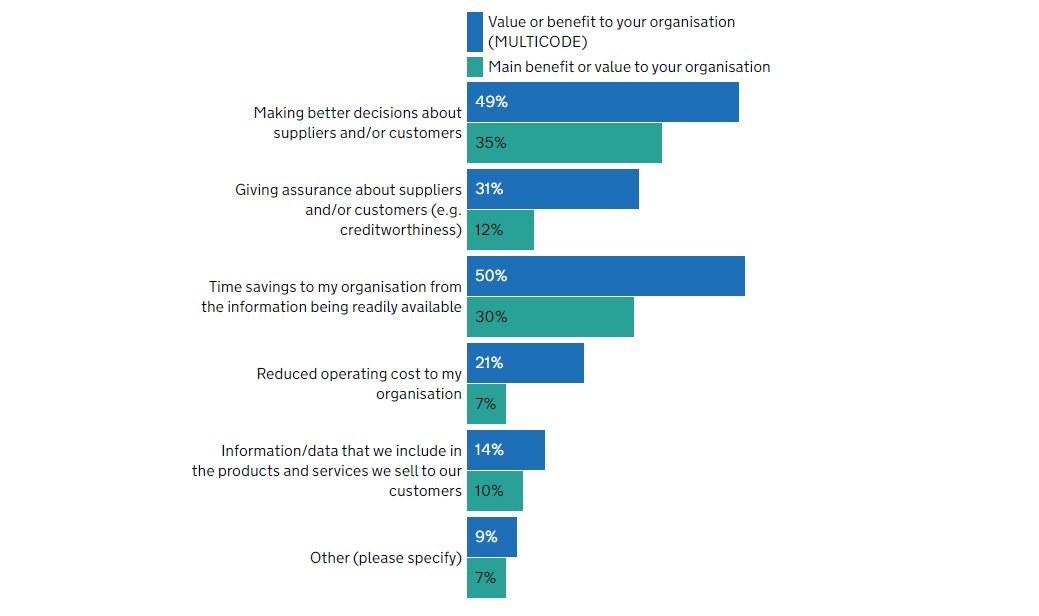

Case study 1: Danske Bank

The Danske Bank case highlighted the crucial role played by anonymous UK registered entities in moving illicit wealth around the globe, and in facilitating international money laundering and corruption. The veneer of legitimacy provided by association with a UK registered company was crucial to $200 billion flowing through accounts of non-resident customers from Russia and other ex-Soviet countries via Danske’s Estonian branch through hundreds of UK registered entities. A 2018 report found that more than half of the 10,000 customers in Danske’s non-resident portfolio had suspicious characteristics. This was one of the largest money laundering scandals in European history. It ultimately led to Danske Bank in 2018 admitting that its procedure for oversight had completely failed and that its money laundering controls in Estonia had been insufficient.

The 2018 report also found that UK registered limited liability partnerships (LLPs) were the preferred vehicle for the non-resident customers. UK LLPs were used in the ‘Azerbaijani laundromat’ from 2012-2014, where USD 2.9 billion dollars was laundered by 4 UK registered LLPs. Similarly, the ‘Russian laundromat’ scheme in 2013-2014 involved 177 customers, many of whom were UK registered LLPs.

29. Typically, these cases see UK entities set up as the holders of overseas bank accounts, or as the owners of assets (e.g. ships) or signatories to contracts. The illicit activity (moving money, weapons or other assets) may not immediately touch the UK’s shores, but it serves to create instability elsewhere, to further the interests of actors hostile to the UK, and/or to help move corruptly-obtained funds into the Western financial system, which may in due course reach the UK. Furthermore, such cases undermine good governance and faith in the UK economy and tarnish our reputation as a trustworthy global economy (see Case studies 2 and 3). [footnote 16]

30. The problem of so-called ‘shell companies’ has been recognised by G7 countries’, who in their joint anti-corruption statement in June 2021 [footnote 17] reaffirmed their commitment to putting in place measures that promote transparency in the beneficial ownership of legal entities. The UK has already played a leading role in this agenda, having been the first G20 nation to establish a public register of beneficial ownership information (via the People with Significant Control reforms delivered in 2016). This data is integrated into the main companies register and was extended to other entities including Scottish Limited Partnerships in 2017.

Case study 2: The FinCEN files

In Autumn 2020, thousands of Suspicious Activity Reports from the US Financial Crimes Enforcement Network (FinCEN) were leaked. The reports alleged that 3,267 UK limited liability partnerships (LLPs) and limited partnerships (LPs) were set up for suspicious illicit purposes by registration agents between 1999 and 2017. In general, ownership of these LPs and LLPs was hidden by registering them with owners that were companies based in so called ‘secrecy jurisdictions’ – where companies can be registered without publicly revealing who owns them. This allowed the UK partnerships to be owned and controlled anonymously and potentially used to launder money.

There are many legitimate reasons for using these types of UK partnerships. For example, LPs are primarily used by the private equity and venture capital sectors as investment vehicles, LLPs are mostly used by professional service firms in the legal and accountancy sectors who value the combination of limited liability and tax transparency for members. However, the same flexible rules governing UK partnerships which are so highly valued by legitimate businesses, can be misused for illegitimate purposes which harm the UK and global economy.

Case study 3: Moldovan Bank Fraud

In 2014, $1bn vanished from 3 of Moldova’s leading banks, much of it through UK companies. $1bn was transferred in just 2 days to a series of UK and Hong Kong registered companies, whose ultimate owners were unknown. A report by Kroll describes how the 3 banks were taken over by new owners in 2012 who appeared to be unconnected. Some owners bought their shares in the banks using funds from UK LPs. The banks then entered into a series of transactions which Kroll says had “no sound economic rationale”. The web of loans emptied them of funds until “they were no longer viable as going concerns”. As a result, the Moldovan state was forced to step in to bail out the banks and protect depositors. Moldova is Europe’s poorest country, and the Moldovan government’s action created a hole in the public finances equivalent to an eighth of GDP.

The use of corporate entities by organised crime groups

31. As recognised in the Integrated Review, [footnote 21] economic crime is a significant threat to the security and the prosperity of the UK and costs the UK economy £8 billion p.a.

32. Economic crime refers to a broad category of activity involving money, finance or assets, the purpose of which is to unlawfully obtain a profit or advantage for the perpetrator or cause loss to others. This poses a threat to the UK’s economy and its institutions and causes serious harm to society and individuals. [footnote 22]

BEIS research valued Companies House data at between £1-3 billion per year in 2018, with financial information the most valuable information to users.

33. Much economic crime is driven by serious and organised crime groups. The Home Office report on Understanding Organised Crime, shows that the total estimated social and economic cost of organised crime to the UK is £37 billion (2015 to 2016). [footnote 23] Serious and organised criminals prey on the most vulnerable in society, and their activities can have a devastating, life-long effect on their victims (see Case study 4). [footnote 24]

34. Enterprises such as supplying drugs and human trafficking which cause direct harm to UK citizens can be facilitated by the use of corporate entities. As a result, Companies House is supporting increasing numbers of Police investigations and helping bring perpetrators to justice.

Case study 4: Companies House support for human trafficking investigations

Organised crime groups involved in human trafficking have been known to abuse the company registration framework. In one case victims were enticed by the prospect of well-paid jobs, were housed in basic, cramped, multi-occupancy accommodation and sent to work long-shifts at factories and recycling plants. They were completely reliant on the organised crime gang for food, drink and shelter and were subject to physical violence and threats when they did not comply.

The organised crime gang also used the victims’ details to incorporate limited companies. These companies were then used to facilitate the opening of further business accounts to be used as ‘mule’ accounts for the rapid dispersion, layering and conversion of criminal property.

The evidence provided by Companies House showed the sophisticated nature of the money-laundering carried out by this network. It also assisted in showing a hierarchy amongst the offenders, the level of financial exploitation of the victims and a timeline of events.

Those convicted were sentenced to over 32 years in prison.

How reform will support national security, combating corruption and fighting organised crime

35. Reform of the companies registration framework will help the UK to better protect itself, respond to the threats outlined in the Integrated Review and address the kind of examples set out above. Reform will enhance the UK’s positive contribution to the global economy, reinforce our standing as a secure and trustworthy place to invest and do business in, and help defend ourselves against the threat of organised crime.

36. The Registrar will be given a new statutory role to maintain the integrity of the register of companies and the UK’s business environment. To carry out this duty, the Registrar will be equipped with stronger powers to query, seek evidence for and remove information from the register.

37. Working with other agencies, new risking capabilities will allow Companies House to stop and query suspicious filings that, for example, follow patterns known to be associated with misuse. Suspicious activity may be identified in several ways including: reports made via the Companies House ‘Report it Now’ function, discrepancies reported by regulated professionals under Money Laundering regulations or members of the public, anomalies in register information identified via cross-checks with other data or internal analysis of patterns or trends in data held by Companies House or law enforcement.

38. A cornerstone of the reforms is the introduction of mandatory identity verification for the vast majority of individuals incorporating or filing with Companies House. This will mean that individuals associated with UK registered entities will have to prove they are who they say they are. It will be much harder to appoint fictitious directors or beneficial owners.

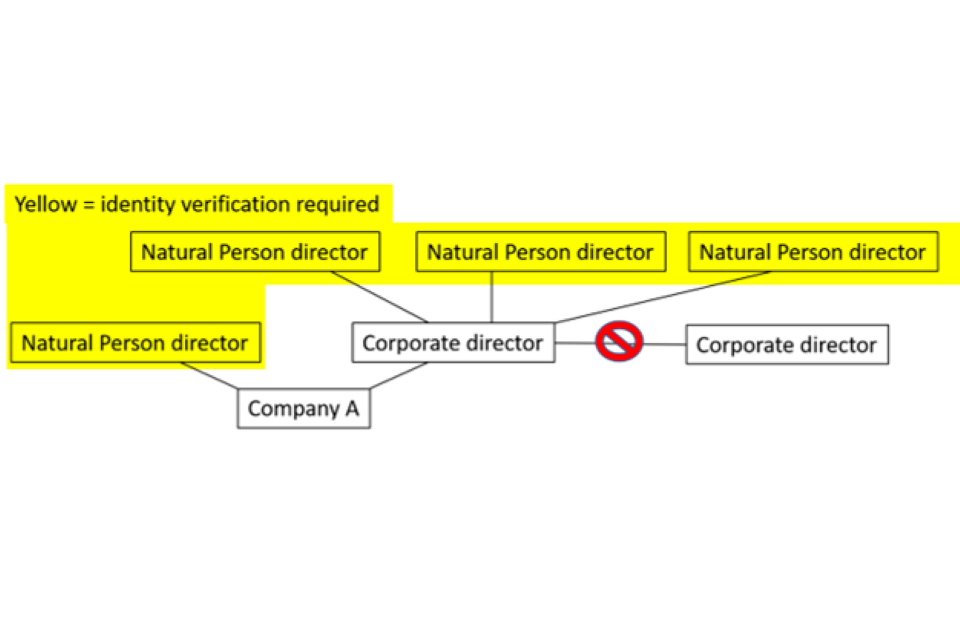

39. The requirement to have at least one fully verified person directly associated with each entity on the companies register, and implementation of new restrictions over corporate directors will make it more difficult to create the anonymous corporate structures demonstrated by, for example, the FinCEN files (see case study 2). In future, companies will be allowed a maximum of one ‘layer’ of corporate directors, which must be based in the UK, and the natural persons directing that corporate director will be subject to identity verification.

40. If an individual fails to verify, the public register will be annotated to show this. This will enable anyone viewing the register to make their own assessment of the integrity and risk profile of those they are researching.

41. Intelligence from law enforcement suggests that those using UK corporate structures for criminal or corrupt activity often use formation agents. If based in the UK, such agents are required to be supervised by HMRC or a professional body under existing money laundering legislation. But there is currently nothing to stop agents based overseas, who may not be subject to equivalent supervision, from making filings with Companies House.

42. In future, agents will be required to evidence that they are adequately supervised before they can register with Companies House and file on behalf of their clients. This evidence will be cross-checked against information from HMRC and the Financial Conduct Authority to ensure its validity. In effect, overseas agents will no longer be able to access Companies House unless at some future date the government determines that any other jurisdiction should be deemed to have an equivalent supervisory regime.

43. Individuals who fail to verify their identity or comply with new requirements under these reforms will be subject to new criminal and civil sanctions. Sanctions will send a strong message that the UK takes breaches of its law seriously and that those who seek to undermine its rule of law and open economy will face consequences.

44. A range of other reforms will improve the quality of the register and close loopholes associated with filings of financial information and People with Significant Control. This will benefit not just law enforcement agencies but businesses conducting customer due diligence checks and independent investigators.

45. In combination, these reforms will deter the kind of misuse seen in the examples given above and make it easier to spot and take action against any such activity in future.

Part 2B: Protecting individuals and businesses from fraud

46. Fraud is the most common form of economic crime. Indeed, fraud has now become the most common crime in the UK, with the pandemic being used as an opportunity by fraudsters to exploit and target potential victims. Fraud can be a devastating crime for individuals and businesses, and it affects approximately one in thirteen people in the UK. [footnote 25] Fraud costs businesses and the public sector £5.9 billion per annum. [footnote 26]

47. This part sets out case studies of frauds that abused the UK corporate registration framework and how legislation reforms and transformation of Companies House will work in concert to reduce them. The use of corporate entities and the companies register in fraud

48. There are a range of ways in which the UK’s flexible framework for company registration and filing has been abused by fraudsters and those committing a range of other economic crimes. Typically, a fraud using companies and/or the companies register will feature one or more of the following:

- the creation of companies specifically to perpetrate fraud

- the use of an individual’s or businesses personal details or address without their consent, including to obscure ownership and control of a company

- filing other false information about a company to lend a veneer of legitimacy

How reform will help tackle fraud

Tackling the creation of companies specifically to perpetrate fraud

49. Criminals can register companies and other entities at Companies House and use the veneer of legitimacy provided by appearance on the companies register to facilitate and perpetrate a range of frauds. These include long-standing problems with so-called ‘phoenix trading’ (Case study 4) which can leave creditors unable to make claims on assets and customers unable to reclaim deposits. Other examples are more recent developments, such as the establishment of companies to fraudulently claim for government support during the Covid pandemic (Case study 5).

Case study 4: Phoenix trading

The practice of phoenix trading and the exploitation of creditors who deal with companies in good faith manipulates the principle of legal identity without liability. Typically, assets are sold undervalue to an associated company with a similar name and common directors. The associated company will continue trading on the same basis, free from debt which has been parked in the old company.

In the recent case of the Insolvency Service v Wallace, 2 individuals were prosecuted for making false representations to the High Court to secure a validation order enabling them to access funds in a frozen company bank account. It is reported that one of the individuals committed fraud in anticipation of the winding up of the same company by diverting £111,000 to a phoenix company. That individual was disqualified as a director for 9 years.

There are existing controls that address phoenix trading, but these only apply once the misconduct is identified through the insolvency regulatory framework.

Case study 5: Using UK companies to defraud the furlough scheme

In 2021, HMRC seized £26.5m in previously claimed furlough cash from the accounts of a series of companies registered at Companies House. An ‘entrepreneur’ registered 4 fake companies that claimed to be an IT services company, a corporate charity, a research hospital, and a religious institute. These shell companies were all registered to a virtual address and each claimed to have dozens of employees and had similar company names. Each company received between £5 and £10m in furlough funding.

In measures announced by the Chancellor in the March Budget 2021, £100 million was allocated for a new Taxpayer Protection Taskforce to crack down on COVID fraudsters who have exploited UK government support schemes.

50. Such frauds are often characterised by fraudsters using registered companies in recognisable ways e.g., registering a company with a similar name to an existing company or at the same virtual address. Through transformation, Companies House will have a more powerful analytical capability to spot such suspicious behaviour and, based on this better data, then exercise its new querying power to obtain further information or report it to law enforcement for further investigation. New gateways for data sharing will facilitate this, alongside Companies House’s membership of cross government law enforcement networks such as the Government Analysis and Intelligence Network (‘GAIN’).

51. Alongside this, all directors, people with significant control (PSCs), and those presenting information on the register will have an account that includes a verified identity and links their appointments in one place. This should make existing legislation easier to enforce. Often company directors are untraceable, making enforcing offences under the Insolvency Act 1986 challenging. Identity verification will ensure there is always a verified natural person associated with an incorporation or a filing – making those individuals far easier to trace.

52. Linking all appointments in one place should also allow consumers to check the register and potentially recognise fraudulent or suspect companies before transacting with them. For example, if the register showed a director associated with multiple companies with similar names which have been created and wound up in quick succession, this could be an indication of fraud.

53. These reforms, complemented by HMRC investigatory powers and new powers for the Insolvency Service to investigate directors of dissolved companies, [footnote 30] will create a more robust framework to combat these types of fraud.

Tackling the non-consensual use of personal details or addresses

54. It is currently possible to register an appointment at Companies House without the knowledge or consent of the person being registered. Companies House has no powers to confirm consent and is legally obliged to register the appointment (Case study 6).

Case study 6: Fraudulent director appointments

In 2020/21, Companies House processed 1,388 applications to remove material related to a director appointment on the register. In the majority of cases, this service is used to remove director appointments that are on the public register where the appointee did not consent to the appointment.

In one instance, a handbag containing identity documents was stolen and the person’s details used to register companies that were then used to open bank accounts. When Companies House removed the person’s details, they were immediately reappointed. In response, Companies House changed its process to prevent a person being reappointed unless they provided evidence under section 1049(b) of the Companies Act 2006.

55. It is time-consuming to remove fraudulent appointments from the register – under the existing legislation a victim must prove to Companies House that they are not the director and wait 28 days before the appointment is removed from the register. In the case of PSC registrations, a court order must be obtained by the victim in order to remove a fraudulent registration – this can be costly and stressful for the victims. [footnote 31]

56. Similarly, it is currently very easy for companies to be registered at addresses without the knowledge of the resident or owner of that address (Case study 7). In these instances, addresses will be used by other unauthorised businesses that take part in scams targeting vulnerable people. During 2020/21, Companies House moved 4,194 disputed addresses to the default address at Companies House, a proportion of which are likely to be a result of fraudulent use of a registered address.

Case study 7: abuse of registered addresses

Recently, Leicestershire Police had warned people to be vigilant to a scam letter claiming to be from Companies House. The scam asked homeowners to confirm the registration of a company using their address; these home addresses had been falsely registered at Companies House without the occupants’ knowledge.

In such cases, unexpected company correspondence can be sent to the residents, including data protection fees, HMRC letters, and notices from Companies House. This can be stressful and require victims to prove their address is not the registered office.

57. These relatively simple but harmful frauds, based on identity theft and manipulation of Companies House’s duty to register properly delivered information, will be far more challenging to carry out in future. Identity verification requirements will reduce fraudulent appointments: registration of a company officer will require a legitimate identity document to be provided and matched to the individual. It will also be more difficult to carry out such frauds via agents, as only anti money laundering-supervised third party agents will be able to register directors (or other officers) at Companies House. These additional verification checks should stop the vast majority of fraudulent appointments from reaching the register.

58. New systems at Companies House will ensure a person who is registered as a director will automatically receive a digital notification informing them of their appointment and giving them an opportunity to challenge it. Companies House will be able to rapidly action any complaints through new querying powers and expanded powers to suppress and remove information. This will mean that anyone whose address or identity is used fraudulently on the register will be able to have it removed from the register in a far more straightforward manner without having to go to court.

59. Finally, there are instances where information held on the register can put an individual at risk of harm, whether that be through fraud or another type of crime. LexisNexis and Cifas have published evidence which suggests company directors are disproportionately likely to be a victim of identity fraud. [footnote 32] It is likely that publicly available information about company directors is used as a starting point for identity theft.

60. Our proposals include the introduction of a mechanism by which individuals can apply to suppress historic personal information that remains on the public record and for which there is currently no power allowing suppression. This will give individuals greater protections over their personal information to safeguard them from fraud and other risks associated with having personal information on the public register.

Tackling other instances of filing false information

61. Criminals may file false information about a company to lend it legitimacy. This can then enable them to perpetrate fraud. In particular, filing false or incomplete financial information on the register can facilitate a range of illicit behaviour. In some instances, companies have been found to have deliberately filed a false set of accounts.

62. In some cases, the company in question has gone further and falsely claimed that their accounts have been prepared or audited by a trustworthy firm of accountants or auditors, [footnote 33] helping to lend legitimacy to fraudulent activity, or painting a false picture of the company’s financial position in order to deceive potential lenders, investors, customers, or suppliers. In such cases it is not untypical to find that the company has claimed a stronger financial position in its Companies House filings in order to impress stakeholders, whilst stating a less strong position in its returns to HMRC in order to reduce its tax liability. Recent work comparing data held by Companies House and HMRC has demonstrated the value that will be gained from more systematic exchanges of data in future (see Case study 8).

Case study 8: filing false or incomplete financial information

In 2019, Cabinet Office, Companies House, HMRC, and the Insolvency Service worked together to tackle the problem of company accounts fraud in a cross-government project. They analysed Companies House and HMRC data across a range of potentially illicit areas including mini-umbrella companies, incorrect filing of micro-entity size accounts, and fictitious companies not filing returns to HMRC. This resulted in the identification of nearly £15m of potential tax fraud and 32,000 companies involved in errors or in improper accounting practice.

63. Through reforms set out in Part 3F, financial information on the register will be more accurate. Introducing a requirement to file a single set of accounts and simplifying accounts filing options should lead to more consistent financial information across different datasets e.g., Companies House and HMRC. This should reduce discrepancies and enable quicker identification of suspicious patterns in company accounts. Alongside this, companies will be required to file enough information to accurately identify which accounting category they belong to, making it far more difficult to abuse the accounting framework and file accounts under the wrong regime to hide income levels. Companies House will then have more accurate financial data which, through increased data sharing capability, can be cross referenced with other data sets e.g., HMRC, leading to more effective identification of fraud.

64. As part of the Accountancy Fraud Sector Charter, the government has been working with the accountancy sector to ensure the reforms can tackle the issue of fraudulent instances of accountancy firms being registered. Mandatory digital filing and i-XRBL tagging will allow anyone to search information on the register much more quickly and easily. Suspicious filings could then be reported to Companies House, who could then engage the new querying power to challenge the filing and, if fraudulent, use enhanced removal powers to remove the information from the register.

Part 2C: Boosting enterprise

The role of the companies register in the business environment

65. The government’s plan for growth sets out a plan to grow the economy across 3 core pillars: infrastructure, skills, and innovation. [footnote 35] BEIS supports this through its strategic priority to boost enterprise and make the UK the best place to start and grow a business. [footnote 36] To achieve these objectives, capture the opportunities arising from the UK’s exit from the EU and to overcome challenges posed by COVID, the UK needs an open and dynamic economy, underpinned by a stable framework for businesses to operate in. The UK is already in a strong position and reform of Companies House will reinforce that.

66. Our quick, simple company incorporation framework is a key factor in the UK’s flexible and attractive business environment. Swift company incorporation allows entrepreneurs, investors, and mature companies to efficiently create the company structures necessary to run effective businesses. Alongside this, publicly accessible company information provides businesses with a wealth of essential information that underpins economic activity in the UK.

67. As set out in the introduction, Companies House plays a fundamental role in boosting enterprise in the economy by facilitating the creation of limited companies and other entities, and making information about them visible on the public register.

68. In 2021, BEIS research looked at business owner’s reasons for company incorporation and the value of different aspects of incorporation. [footnote 37] The total value of company incorporation to owners of limited liability companies with 0 to 9 employees in the UK, which represents approximately 89% of limited liability companies, was estimated to be approximately £9.6 billion per year. Of this, the greatest proportion of the value is associated with limited liability, accounting for around 80% of the benefit to business owners.

69. The companies register is used for a wide range of business purposes (see Chart 1), informing many business and lending decisions. Research has valued the data to users of the companies register at £1-3 billion in 2018, generating a range of benefits for businesses (see Chart 2). Key benefits included obtaining assurance and making better decisions about suppliers and/or customers and time savings. Direct users attributed the greatest value to the provision of financial information (55% of the total value) and attributed a further 41% of the value to basic company information. PSC information accounted for approximately 4% of the total value – although this increases to 13% for ‘high use’ users. The value of the register will have grown subsequently as the use of the register has continued to increase.

Chart 1: Use of Companies House data [footnote 38]

Chart 2: Beneficial outcomes of Companies House information and data

70. Organisational transformation will strengthen the contribution of Companies House to the UK’s business environment, make its services even more user friendly and bring direct benefits to companies and other entities registered at Companies House. The information on the register will become more reliable, accurate, and transparent, bringing wide reputational benefits to businesses on the register, better data for company credit scores and a reduced administrative burden. Alongside this, risks to company directors and owners from having their personal information on the public register will be reduced – as set out in the previous part – enabling them to run their companies with more confidence.

A more reliable register

71. The central outcome of these reforms will be a significant increase in the reliability and accuracy of the information on the register. Identity verification, powers to query and reject information and improved financial information will work together to make register information more useful. Identity verification will mean users have more confidence that company officers on the register are who they say they are. Where register information is wrong, inaccurate or fraudulent, the Registrar will be able to query and, in some cases, remove that information. With increased data sharing capabilities, Companies House will be able to cross reference its data with other government data sets and identify inconsistencies more quickly.

72. We envisage that, through these reforms, the information on the register will be more accurate for businesses to use and therefore enable better business decisions. Appearing on, and having access to, a more reliable register benefits businesses in a number of ways. The research outlined above suggests that businesses value the act of incorporation not just for the limited liability it bestows, but because appearing on the companies register helps businesses secure contracts and strengthen their overall reputation and credibility. [footnote 39] Increasing the overall reliability of the register should enhance these reputational benefits for all registered companies and directly benefit businesses who use register data in their own products.

How higher quality register data benefits business

- Reforms to the register – lead to

- Higher quality register data – which leads to

- More accurate information for businesses to use – which leads to

- Better business decisions

73. Certain industries are likely to see direct benefits from the new information provided by companies under these reforms. For example, professions regulated by the anti-money laundering regulations, such as legal and accountancy firms, will be able to take more assurance from the register, supporting their own due diligence before accepting new business clients.

Access to credit

74. Improvements to information on the register should bring benefits to companies seeking credit. This a vital element to enterprise – the World Bank has highlighted availability of credit data as a fundamental component of SME financing. [footnote 40] Data on the Companies House register is an important element of a company’s credit score – the British Information Providers Association (BIPA) recognises Companies House data as a fundamental component of the work of credit reference agencies (CRAs).

75. CRAs facilitate billions of pounds worth of business transactions by providing creditors with financial information about potential clients. These creditors include banks providing loans and those providing trade credit. Quick access to credit is vital to support the SME sector in recovering from the impact of COVID-19, with 45% of SMEs applying for external financial support in 2020, up from 13% in 2019. Trade credit is also vital to the SME sector: 37% of SMEs used trade credit in 2020. [footnote 41] More reliable register data should help CRAs form more comprehensive and accurate credit scores, meaning creditors can take informed decisions more quickly, benefitting business access to credit across the economy.

Better financial information

76. Research has shown that direct users of the register attribute most value to the financial information on the register (55% of the total value). We are bringing forward a number of reforms – detailed in Part 3F – to make this data more reliable, useful and searchable.

77. We will simplify the framework for filing accounts with Companies House by streamlining the complex set of filing options for small companies. At the same time, we will level the playing field so all businesses file a set of useful financial information, and Companies House will have the power to reject accounts that do not meet certain statutory requirements. This will reduce the fraudulent abuse of UK accounting frameworks and provide more reliable data for businesses doing due diligence on their clients and suppliers.

78. We will require full iXRBL tagging of accounts information on the register and reject accounts that do not meet the required tagging standard. At a stroke, this will make company accounts information on the register more complete, accessible and, crucially, it will be easier for organisations to search and analyse the data in bulk. This will provide a wealth of insight on the economic performance and benefit certain industries that use Companies House data as a product. We will also explore how Companies House can display the financial information on the register more effectively. This will allow users to quickly obtain the information they need, overcoming the challenge of searching through individual sets of accounts and allowing users and researchers across a range of businesses to access better data more quickly.

A renewed digital service

79. Companies House aims to become a fully digital organisation. Transformation of systems and processes will bring business benefits through streamlining and digitising processes and improving the user experience.

80. Companies House digital services already work well, with 91.4% of users taking up digital services in the last year. However, many that were pioneering services when they were first developed are now ageing. The reforms will see a transformation of Companies House services, replacing ageing services and supporting infrastructure with new ones. This will mean systems across the register are quicker and easier to use, saving businesses time when transacting with Companies House.

81. Users of digital filing services typically save time and effort and are more compliant. Users will be able to do what they need to do quickly and correctly – making creating and maintaining a compliant company an even easier task. Company directors will have a single account linking all of Companies House functions into one place.

82. Where users set up an account, all their appointments will link to a central account, helping manage their affairs more easily. This will mean quicker and easier filing, reducing the administrative burden of filing at Companies House, allowing company directors to focus on running their businesses. This translates into less effort and therefore lower costs, and more data appearing on the register in a timely manner, once again leading to a register that is more up to date and more accurate.

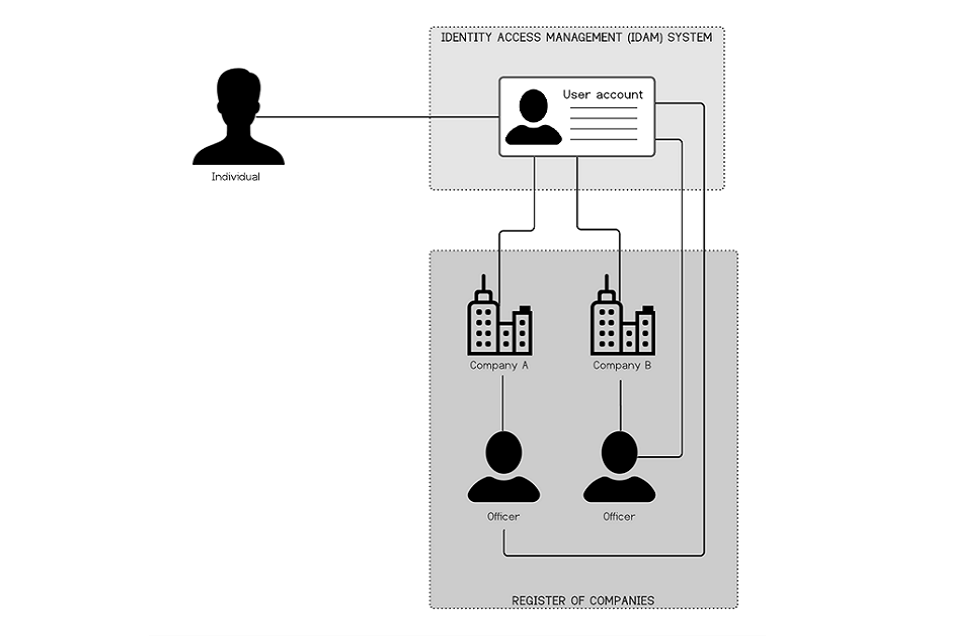

How the Companies House account will link multiple appointments across the register

Individuals will have one account linking all their roles across the register. Where an individual has more than one role or is registered with multiple companies as a director or a PSC, all that information will be contained in one place on the register.

Part 3 – The reforms in detail

Part 3 sets out the reforms in detail, beginning with the transformation of Companies House, followed by the registrar’s new statutory powers and responsibilities, new requirements on identity verification, increased powers to share data, enhanced privacy mechanisms, and finally reforms to how companies report their financial information to Companies House.

Part 3A: Transforming Companies House

83. The objectives set out earlier in this document will be achieved not just through legislative reform but through a fundamental operational transformation of Companies House. In its systems, processes, and capabilities, Companies House will change to reflect its new role in the economy and its responsibility to help achieve the government’s priorities in national security, anti-corruption, tackling fraud and boosting enterprise. The changes will comprise the most fundamental change to its purpose and role since its creation; indeed, since the creation of the role of Registrar in 1844.

84. To deliver the government’s ambition, every aspect of Companies House will be transformed: skills, culture, operating model and services. This part summarises some of the key elements of the transformation.

85. In terms of skills and culture, the organisational structure of Companies House is still very functional, and many job roles are administrative and paper based. With updated digital systems for both customer services and back office automation, these roles will decrease and there will be a greater emphasis on analytical work to maximise quality data. The result will be a more innovative and flexible organisation with different roles requiring different skills.

86. In terms of operating model and services, Companies House currently relies on legacy systems which are ageing, some having been built over twenty years ago using technologies which are increasingly difficult and resource intensive to maintain. They cannot provide the robust foundation needed, or be adapted to deliver against modern standards and ensure Companies House can continue to meet the rising demand for its data and services.

The transformation programme

87. The transformation of Companies House is already underway. £20 million is being invested in 2021-22, with a further £63 million announced up to 2024/25 at the most recent Spending Review. The programme features a move to a functional model based around key services, supplemented by new investigation and intelligence functions, all underpinned by further digitisation and cultural change (see Box 1).

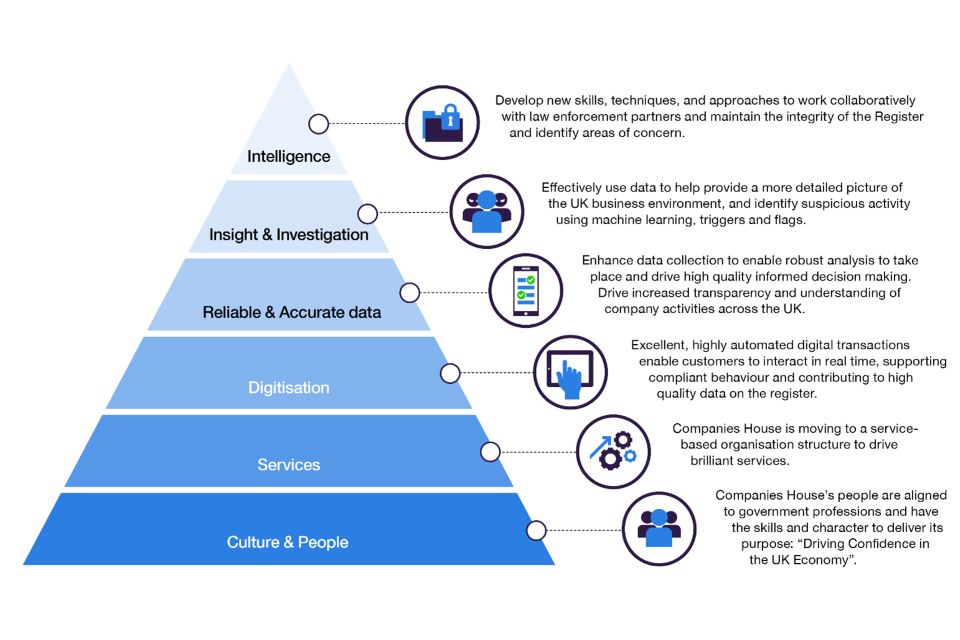

Box 1: Key elements of the transformation programme

Text of box 1: Key elements of the transformation programme

- Intelligence: develop new skills, techniques, and approaches to work collaboratively with law enforcement partners and maintain the integrity of the Register and identify areas of concern

- Insight and investigation: effectively use data to help provide a more detailed picture of the UK business environment, and identify suspicious activity using machine learning, triggers and flags

- Reliable and accurate data: enhance data collection to enable robust analysis to take place and drive high quality informed decision making. Drive increased transparency and understanding of company activities across the UK

- Digitisation: excellent, highly automated digital transactions enable customers to interact in real time, supporting compliant behaviour and contributing to high quality data on the register

- Services: Companies House is moving to a service-based organisation structure to drive brilliant services

- Culture and people: Companies House’s people are aligned to government professions and have the skills and character to deliver its purpose, driving confidence in the UK economy

88. The transformation programme will deliver against the following goals in the Companies House 5 year strategy: [footnote 42]

- Registers and data that inspire trust and confidence

- Maximise the value of Companies House registers to the UK economy

- Economic crime combatted through the active use of analysis and intelligence

- Brilliant services giving a great user experience

- A culture that enables people to flourish and drives high performance

- Value delivered through efficient use of resources

89. Projects within the programme will transform interactions with customers and internal structures and in doing so will be more effective, efficient, and adaptable to future change. Transformed digital services utilising automation and new technology will help users to get it right first time. Services will meet usability and accessibility standards such as those demanded by the Government Digital Service (GDS).

90. Less paper and manual data processing will free up staff time, and data will be stored in ways that make it more machine-readable and hence easier to access and process, both internally and by external users including law enforcement partners. This in turn will facilitate a better understanding of the UK economy and economic trends, providing better knowledge to shape better business decisions.

91. At the same time, development of core components of Companies House data strategy, such as a ‘data lake’, will ensure that data is stored so that it can be analysed to provide intelligence for fighting crime – an example of current investment enabling many future benefits.

92. Investing in identity and access management provides the underpinning service that will be vital to exercise future powers under register reform to carry out identity verification. In the first instance, prior to legislation, the technology will deliver a Companies House account service enabling users to sign in once for a number of services as opposed to the multiple logins currently required. This in itself is expected to provide better data for cross-checking, reducing avoidable contact and increasing customer satisfaction.

93. The small number of interactions which cannot be carried out digitally will further reduce, notably with the introduction of a facility for digital notification of insolvency events – something which will boost digital capability, provide vital information more quickly and will remove the substantial risks in this area associated with data entry error. Companies House will ensure standards of accessibility are maintained and provide assisted digital support.

94. Not as visible but equally important is the development of infrastructure components that will form the basis of future services. Where applicable, Companies House will integrate GOV.UK services such as Pay and Notify but in other cases core components will need to be developed in-house.

95. Companies House’s transformation programme will address all of these requirements and includes extensive work to upskill areas of the organisation, implement smarter ways of working, enhance the organisational design, and deliver new capabilities and services to achieve the largest transformation in the history of Companies House.

96. None of the transformation of Companies House, nor even the steps towards it, would be possible without its people delivering in a variety of capacities, be that operational, technical or supporting roles. Recognising this, extensive effort has gone into determining the right organisation design for Companies House and that will come into fruition with the initial implementation of a service based model. People in Companies House will help shape changes to roles and organisational structure will change, embracing new ideas, encouraging innovation, and developing the skills needed to achieve the vision whilst still valuing experience.

97. The Companies House transformation will complement legislative reform to enable Companies House to achieve its vision of being the most innovative, open and trusted registry in the world – with brilliant services delivered by brilliant people. Achieving this vision will drive progress across national security, economic crime and boosting enterprise.

Part 3B: The role and powers of the Registrar of companies

98. Alongside the transformation of the organisation, the most fundamental changes arising from these reforms will be to the powers and statutory role of the Registrar. Companies House will no longer be a passive administrator of company information but will become a much more active gatekeeper over company creation and custodian of more reliable information on the register.

99. In 2020, the government committed to introducing a new discretionary power for the Registrar to query and check information submitted to her. The new querying power is a cornerstone of our wider reforms and will help to deliver a more reliable register, underpinning business and lending decisions and tackling fraudulent filings.

100. At the same time we undertook to consult in more detail on the new querying power. This consultation was published in December 2020 and closed in February 2021. [footnote 43] Respondents to this consultation broadly agreed with these more detailed proposals. A full response to that consultation can be found in Annex 2.

101. This part sets out the new role the government proposes to give the Registrar, and the querying and other new or expanded powers that will flow from that new role.

Role of the Registrar

102. The Registrar’s existing role is to register company information and to make it available for public inspection. In the 2019 consultation and government response we outlined our intention to give the Registrar a greater role in assisting the fight against economic crime, and to provide a legal basis for this change of function. We consider that this new function should be future-proofed and so no longer propose linking this solely to economic crime.

103. Instead, we propose introducing a new function for the Registrar which provides her with a new role in promoting and maintaining the integrity of the register, thereby enhancing the UK business environment; the new role will capture economic crime and other activities that may undermine the integrity of the register. This function will be supported by new powers which will enable the Registrar to carry out her new role, including the new querying power and greater data sharing powers.

104. The new role is specifically intended to increase trust in the UK business environment by increasing the accuracy of the information held by the Registrar. While the Registrar is far from wholly responsible for the UK business environment, maintenance of a more reliable register, expanded powers to tackle abuse and greater data sharing powers will contribute to ensuring that the UK remains a trusted place to do business. Providing a clear statutory function for the Registrar to promote and maintain the integrity of the register will provide more flexibility for the Registrar to carry out the new activity we propose under register reform and help to prevent corporate misuse. We consider this new function to be an essential element for achieving our desired aims, and in ensuring that should new threats arise in the future, Companies House is able to respond to them in an agile way.

A new querying power

105. Companies House is currently required by law to accept information if it is ‘properly delivered’ and has very limited powers to correct or query information if it suspects that something submitted to it is erroneous or fraudulent. Providing a power to reject and query new filings, as well as to query information already on the register, will benefit business and provide more assurance that the register is accurate, as well as improving the integrity of the companies register. It will be applied where information is identified as potentially fraudulent, suspicious, or might otherwise impact upon the integrity of the register. The new querying power is vital to transforming the role of Companies House from a passive to a more active one, that is better equipped to tackle fraud and other economic crime, helping to maintain and improve the integrity and reputation of the UK’s business environment.

The scope of the querying power

106. The key principles under which the querying power will operate are as follows:

- The first principle is that all information supplied to the Registrar or information already on the register will be in scope of the new power. The new power will apply to all filings and the Registrar will be able to use this power to query information pre- and post-registration and, in some cases, to remove information already registered.

- Secondly, the power will be used on a discretionary basis. The Registrar will not be under any legal obligation to exercise the power in all circumstances or specific/unique circumstances. This is because we consider that it would be disproportionate for the Registrar to have to monitor millions of filings to identify every error or anomaly.

- The third principle is that the registrar will exercise the power using a risk-based approach. Stakeholders agree with this approach. A risk-based approach of this kind is common in the public sector and business, for example, in the requirements for financial institutions to undertake due diligence on their customers. This will ensure that the use of the power is proportionate and uses resources in an efficient and targeted way. Under the risk-based approach, where issues are highlighted to the Registrar, querying will be prioritised in the cases that, in the Registrar’s view, present the biggest risks to the integrity of the register and the quality of information it holds. Exercising the power in this way will help to ensure that it will not inadvertently focus on legitimate transactions.

107. Companies House will require additional resources to handle queries and potential complaints. The purpose of the risk-based approach is to be proportionate, aiming to use resources in an efficient and targeted way. This approach also future-proofs the use of the power as it enables the Registrar to respond to changing circumstances and risks. If we were to set certain parameters now restricting the scope of application, we may not be able to respond to future threats and a changing risk environment.

108. In order to prepare for these changes, Companies House is developing its systems to improve its ability to detect suspicious activity and is building an Intelligence Hub which will identify potential risk factors which might lead to a query. It will also work closely with other agencies on current risks and this will inform prioritisation of queries.

Exercise of the power

109. Pre-registration, the new power will mean that Companies House will no longer be obliged to accept documents that are delivered where there is reason to query the information provided. Where a query is raised pre-registration, the filing will be rejected, and a reason provided. The entity will be able to re-submit the filing, ensuring that the query has been addressed, and supplying evidence if it is required. Should a filing be re-submitted with the query remaining unaddressed or not resolved satisfactorily, it will continue to be rejected.

110. This approach means that information that may affect the integrity of the register, for example because it is erroneous or suspicious, will be less likely to make it on to the register in the first place. It will also help businesses who submit something in error that is picked up and rejected by the Companies House, ensuring that filings which make it onto the register are more accurate.

Process flow for the querying power exercised pre-registration

1. Filing sent to Companies House.

2. Risk flags are raised.

3. Registrar rejects the filing and gives a reason for rejecting.

Either:

4Ai. Filing is resubmitted to Companies House with evidence that resolves concerns.

4Aii. Filing is now accepted onto the register.Or:

4Bi. Filing is not provided to resolve concerns.

4Bii. Filing is rejected again.Or:

4Ci. Filing is resubmitted to Companies House with evidence that is not sufficient to resolve concerns.

4Cii. Filing is rejected again.

111. Post-registration, when a query is raised, the recipient entity will have 14 days to respond and provide evidence to support the response. In order to mitigate the risk that an entity is unable to deliver the evidence required within that period, the Registrar will have a discretion to grant an extension to the time limit where she is satisfied that this is appropriate.

112. Companies House remains committed to providing a smooth and quick process for those submitting information to it, and the querying power will be used sparingly and in line with evidence or risk assessments. A query might be instigated either from information within the Registrar’s own knowledge or because of a concern raised by a third party. The outcome of a query will depend on the response (or lack of response) received.

Non-compliance

113. Should the entity fail to respond to a query, or fail to provide sufficient evidence in its response even after being asked for more, the Registrar will be able to take a number of actions, including if appropriate imposing a sanction upon the entity. A range of sanctions are being considered.

114. We consider that a range of sanctions will help to incentivise compliance, as well as ensure that the Registrar has the appropriate flexibility to assist her in maintaining the integrity of the register. Stakeholders responding to the December 2020 consultation provided a number of suggestions for potential sanctions, and those that we are considering include these suggestions.

Evidence

115. Guidance will be produced to help companies understand how and why the power might be used, and to provide examples of appropriate evidence. Given the variety of matters that might be queried, and the wide range of potential evidence that could be produced, we consider that it will be impractical to set out a definitive list of acceptable evidence. This will provide flexibility for both the Registrar and for companies or other entities whose information has been queried.

Application of the querying power to company names

116. There are certain controls on company names already in place; names cannot be the same as, or too similar to, an existing name, and certain terms are restricted (e.g. implying a connection to the UK government or using a sensitive word or expression).

117. However, stakeholders have told us that there are circumstances where there is a need to query and reject names that pass the tests as they stand now. Companies House has limited powers to prevent a name from being registered or to act once it has been; a regular source of criticism, impacting on the UK’s reputation as a good place to do business.

118. We envisage the new querying power might be used, on a risk-based approach, where a proposed, or registered, name may be part of a campaign to target a company, organisation, or individual with whom the applicant has no connection, where the name of an international organisation or institution is being used (e.g. a bank) without permission, or where there is intelligence of fraud or other criminal activity.

119. Companies House will take a proportionate approach which is intended to strike a balance between maintaining the current speed of registration and safeguarding the integrity of the register. Most companies will continue to be registered without a query being raised.

120. Where Companies House queries a registered name, and evidence to satisfy that query is not received or is unsatisfactory, then it will also have the power to direct the company to change its name within 28 days, with power to change the name to its registered number (or an appropriate alternative) should the direction be disregarded. The company will have the ability to apply to court to set aside the direction, as is currently the case.

121. Companies House will also have the power to change a company’s name to its registered number where it has directed a change of name under existing powers (effectively aligning the existing with the new power). [footnote 44]

122. The government has also been considering the impact of these reforms on the role of the Company Names Adjudicator (CNA) [footnote 45]. While we envisage that some of the cases the CNA currently handles will be picked up by the Registrar of Companies using the new querying power both pre- and post-registration, we believe there is still a clear role for the CNA to continue to deal with cases which require an adjudication to be made between 2 parties following an objection to a registered company name.

123. We believe the scope of the cases which the CNA should be able to consider ought to be expanded slightly. At present a company can avoid a challenge to its name simply on the basis that it is already trading under that name, even if in doing so it is illegitimately targeting another party who has legitimate goodwill in it (a so-called ‘trading defence’). This can clearly be abused by an unscrupulous company. We would like to reframe this defence to be subject to a demonstration that the trading is being conducted in accordance with honest commercial purposes, a concept used in intellectual property law.

Other changes to the Registrar’s powers

124. The government also consulted on proposals to reform some of the Registrar’s existing powers. This included greater powers for the Registrar to remove information from the register, and to close current loopholes including the rectification of registered office address processes. Stakeholders were in broad agreement with our proposals. As we have explored the changes that we need to make, we have also identified other matters that we believe need to be addressed.

125. We intend to make changes to the proper delivery requirements, including providing that a filing may be rejected. This may either be under the new querying power or a new, specific power to reject documents that, in the Registrar’s opinion, may cause harm to the register, even where it meets all other proper delivery requirements. We will expand the Registrar’s administrative removal powers to provide more flexibility and assist in the aim of increasing the accuracy and reliability of the companies register.

Removal powers

126. The Registrar currently has very limited powers to remove material from the register; this limited scope is a source of stakeholder complaints, as well as affecting the integrity of the register and the UK’s reputation as a good place to do business. The Registrar can, for example, administratively remove a fraudulent director appointment on application, but cannot remove a fraudulent People with Significant Control (PSC) registration. In this example, an individual must secure a court order to remove the fraudulent PSC appointment from the register; the cost of which may deter such applications.